Making Life Better? 2024 Communications and Remote Sensing

This is another two-parter, with this part being part 1, which is a general scan of some of the communications and remote sensing satellites and services deployed during 2024.

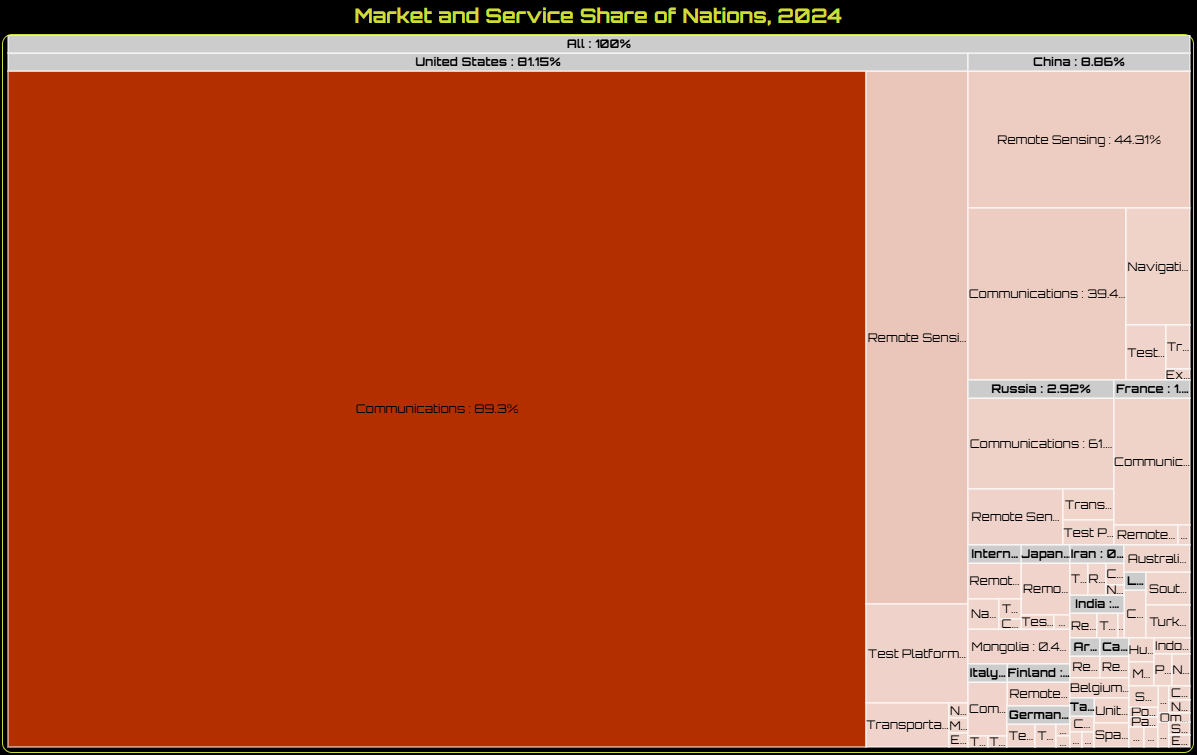

In part 2 of 2024’s “The Ill-Defined Space Spacecraft Market and Service Analysis,” I focused on spacecraft services from four nations: China, France, Russia, and the United States. Within that analysis, I noted:

Over 81% of the spacecraft deployed from the four nations had communications payloads, specifically for internet relay, ship tracking, and cellular communications. Satellites with remote sensing payloads (infrared (maybe), optical, weather, and radar) took ~11%.

I didn’t highlight that for each of those nations, the placement of markets served was the same (excepting China)–communications and then remote sensing spacecraft in a distant second. For China, remote sensing was first, with communications close behind.

Those served markets seem very 1990s.

Give the People What They Want

Although, the type of communications services and remote sensing products offered in 2024 will be very different from those provided in that decade. In shorthand, much of the early 1990s seemed to consist of government spacecraft deployments. However, commercial satellite deployments grew during that time. In theory, the growth for either decade occurred because consumers' lives were improved in some way. Satellite deployments, orbits, etc. likely didn’t and don’t matter to the “normies.” What probably matters more in their decision-making is availability, convenience, utility, and cost.

Perhaps familiarity is also a consideration because, as noted above, satellite communications services were and still are a popular consumer option (although less so in 2024, with the growth of wireless communications).

For example, space communications in the 1990s relied generally on satellites in geosynchronous orbit, typically for broadcasting (including direct-to-home) only. If a person lived in the middle of Wyoming, satellite television offered more entertainment and information for far less than the cable company (which may or may not have even been available). The local and free over-the-air broadcasts likely paled in comparison, and reception might have been an insurmountable challenge for some residents. For those residents seeking basic entertainment, or even more than the local option, DTH improved their lives.

A few examples of other communications services (Globalstar, Iridium, Teledesic) attempted to gain market share. Iridium died, then started again. Teledesic, however, never became operational. But all were communications businesses that used space to serve customers.

Similarly, Earth observation satellites existed in the 1990s, but most were government-run. A few companies deployed commercial versions, but almost all used optical sensors. U.S. companies had the dubious bonus of being limited to delivering products of lesser quality to their non-government customers. Great for their competitors but not so much for U.S. companies. And, like in 2024, the biggest imagery customers still appear to be governments. Regular consumers didn’t seem to have an appetite for imagery. It still seems that way today.

What a Difference Thirty+ Years Makes.

Again, the markets focused on seem similar. However, the scale of satellite deployments in the last several years to serve those markets is impressive. A few years in the 1990s might have exceeded 100 spacecraft deployments. But by 2024, spacecraft deployments almost reached 3,000–for the year. Even when SpaceX’s Starlink satellite deployments were excluded, spacecraft deployments for 2024 still exceeded 800.

COMMUNICATE

Commercial markets served by communications satellites reflect the consumer demands of the period–television entertainment in the 1990s and global internet access in the 2020s. Of course, other types of communications businesses were exploiting space in the 1990s. Better, the business case for either service (terrestrial television and internet) was already established. The service delivery technologies merely differed from their Earthbound counterparts.

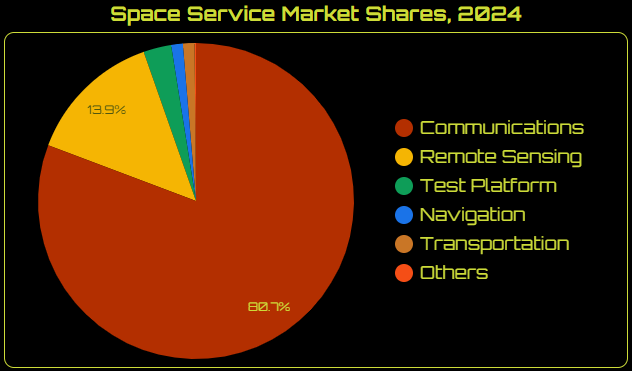

However, the plethora of communications services in 2024 demonstrates that if companies perceive a need, they will try to exploit it. In either decade, they used space technology to make people’s lives better/more comfortable. It’s just that in 2024, companies used a lot more communications satellites. About 81% (nearly 2,240 spacecraft) of 2024’s spacecraft deployments were for some kind of communications service.

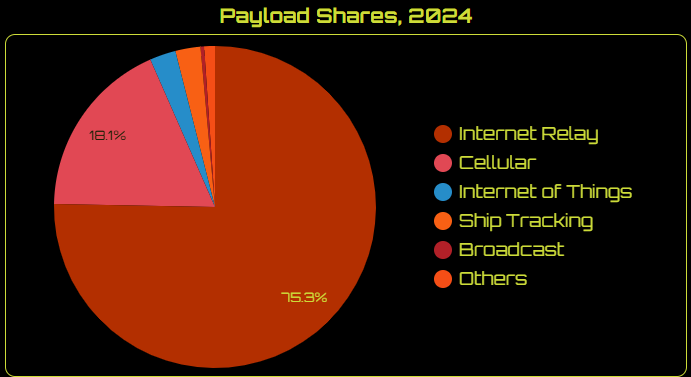

Most of those communications satellites (nearly 1,700) were deployed to basically be network routers in orbit, providing subscribers with internet access. In 2024, SpaceX deployed almost 94% of the satellites providing that service. Genesat, a Chinese company, deployed about 3%, followed by OneWeb (Eutelsat) at 1%, and China Satnet’s Guowang at nearly 1%.

A second type of communications service–cellular communications–is seeing satellite deployment growth. Cellular communications had the second-highest number of deployed spacecraft in 2024 (over 400), with over 98% deployed by SpaceX. About 1.5% were deployed by AST Spacemobile. Cellular from space is a weird one since terrestrial cellular communications are a big, established market. SpaceX, in particular, has dedicated hundreds of satellites to provide cellular connectivity (also suppressing possible competitors). But, the current state of the art appears to have some compromises on the consumers’ part.

For example, some services require payments in addition to the monthly cellular bill. They must have a clear view of the sky for the service to work. It is currently only for texting. There’s also the reasonable possibility that consumers might see their current terrestrial cellular service as good enough without the compromises imposed by the cellular constellations. This is not to say there’s no market for space-provided cellular connectivity, but to note that the market is limited.

Both ship-tracking and internet of things (IoT) services deployed nearly 60 satellites in 2024, about 2.5% (each) of all communications spacecraft deployed that year. For ship-tracking, considering the utility of the service and the hundreds of thousands of ships with tracking transponders, the number of satellites deployed to provide the service seems low. However, terrestrial ship-tracking technologies were available long before satellites started providing the service, and the low number of ship-tracking satellites acknowledges the system’s overall effectiveness.

Say “CHEESE!”

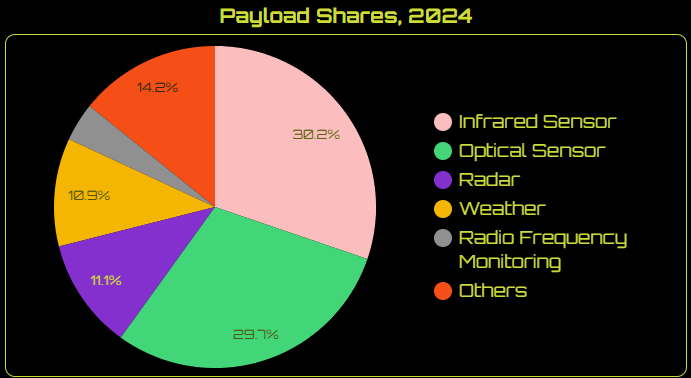

As for remote sensing, for all the visibility and humble brags from the companies serving the markets, it’s not clear to me that consumers are increasingly using their products or services. I know that I barely use any remote sensing products. I even keep the imagery layer turned off in Google Maps because it’s more distracting than helpful. If I use it, it’s usually for buying or renting a home, looking at potential neighborhoods. Maybe I’m the only one?

Despite that apparent general consumer deficit, 14% (over 400) of all of 2024's spacecraft deployments had a remote sensing payload on board. About 30% of those MIGHT have been providing infrared data, with over 90% of infrared satellites deployed for the National Reconnaissance Office. Hence, the “MIGHT” is because those missions are classified, and I have no genuine need to know (despite having a Signal number) what kind of payloads are on the NRO’s satellites.

29% of the remote sensing satellites had optical payloads, with 31% of those deployed by the U.S. company Planet. China’s People's Liberation Army deployed the second-highest share of optical satellites–an estimated 11%- and Chang Guang Satellite Technology company deployed about 9%.

Satellites with radar payloads accounted for nearly 12% (40+) of all remote sensing satellites deployed in 2024. The company deploying the most satellites to provide radar-based products and services was Norway’s IcEye at 20% (9). China’s PIESAT had the second-largest share of radar satellites, deploying nearly 18% (8). The U.S. company Capella and the Japanese company Synspective tied for the next highest share at 6.7% (3) each.

That general scan of some of the communications and remote sensing offerings and the number of satellites used to provide them will allow us to look more closely at some of the services that might be increasingly useful to customers. Some companies are starting to address those needs, but others have yet to be discovered and discussed.

Until next week!

A lot of time and research goes into this general information, as well as unpublished but available higher-fidelity data. If you’re interested in a consultation, please contact me through LinkedIn.

If you liked this analysis (or any others from Ill-Defined Space), please share it. I also appreciate any donations (I like taking my family out every now and then). For the subscribers who have donated—THANK YOU from me and my family!!

Either or neither, please feel free to share this post!

Comments ()